Chinese PV cell and module prices are rising — but the real driver isn’t policy or commodities.

It’s balance sheets.

Recent public disclosures show that seven of the eight largest listed Chinese PV cell and module manufacturers have now recorded two consecutive years of massive losses and risk Special Treatment (*ST) designation. If these losses extend to three consecutive years through 2026 — access to equity markets and bank financing will be seriously restricted, and consolidations and bankruptcies will follow.

For perspective, LONGi alone has accumulated more than USD $2 billion in losses over the past two years.

This is not cyclical volatility. It is sustained structural stress caused by selling below cost into global markets like Canada.

Scale does not guarantee resilience.

Market share does not equal liquidity.

And negative cash flow cannot persist indefinitely.

The pressure in 2026 is clear: restore margins, restore cash flow, stabilize balance sheets.

2026 marks the beginning of a structural reset driven not by policy, but by survival.

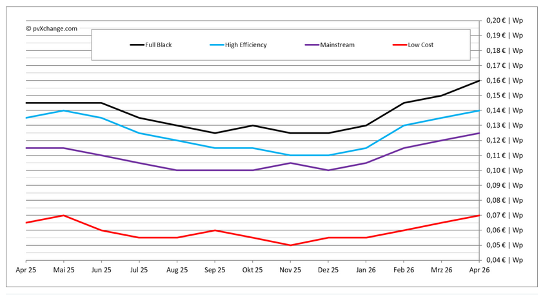

PV cell & module price increases are not opportunistic — they are necessary. Chinese TOPCon module prices have risen 13% in the last three weeks alone and are 30% higher than their low in December 2025.

The financial pressure that Chinese companies are facing does not apply to BAUER Solar. BAUER Solar GmbH is a debt free, profitable German corporation that does not use any Chinese components. While BAUER’s pricing going forward may be affected by raw materials, BAUER’s pricing overall will remain stable as the gap closes with rising Chinese prices.

If you haven’t been buying BAUER because the Chinese prices are so cheap, those days are over.